As 2026 unfolds, the global container shipping market is revealing a transformed capacity landscape. According to the latest data released by Alphaliner on January 4, 2026, the total number of operational container ships worldwide has reached 7,498, with an aggregate capacity of 33.69 million twenty-foot equivalent units (TEU).

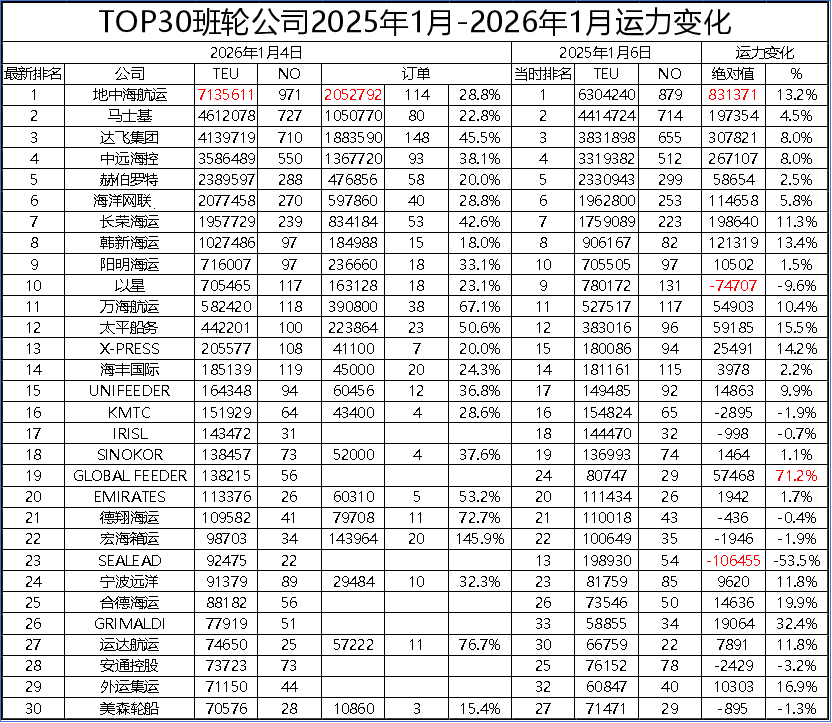

In the updated global shipping line capacity rankings, Mediterranean Shipping Company (MSC) maintains its dominant position with a capacity of 7.136 million TEU, widening its lead over second-place Maersk (4.612 million TEU) by 2.524 million TEU. CMA CGM Group follows in third place with 4.14 million TEU. Rounding out the top ten are COSCO Shipping, Hapag-Lloyd, Ocean Network Express (ONE), Evergreen Marine, HMM, Yang Ming Marine Transport, and ZIM Integrated Shipping Services. Collectively, these top ten carriers control 28.348 million TEU, accounting for 84.1% of global capacity, maintaining the same market concentration level as one year ago.

Over the past year, the combined capacity of the top 30 global shipping lines increased by 2.197 million TEU, representing a 7.5% growth rate and capturing 97.8% of the total global capacity expansion during this period. MSC led all carriers with an increase of 831,000 TEU, marking a 13.2% growth rate, while CMA CGM followed closely with a capacity gain of 308,000 TEU. In terms of growth percentages, GLOBAL FEEDER topped the list with an impressive 71.2% increase, with GRIMALDI, Heung-A Shipping, Sinotrans Container Lines, and Pacific International Lines also recording growth rates exceeding 15%. Notably, Hai Ling Shipping experienced a significant capacity reduction of 106,000 TEU year-over-year, while ZIM Integrated Shipping Services also saw a decrease of 75,000 TEU.

Regarding newbuilding orders, 2025 witnessed a record-breaking year for global container ship orders, with a total of 645 vessels ordered, representing over 5.1 million TEU. As of the latest data, the global orderbook exceeds 1,165 vessels with a combined capacity of approximately 11.3 million TEU, accounting for 33.5% of the existing fleet capacity. The top 30 shipping lines hold 89.3% of these orders, indicating that newbuilding activities remain concentrated among industry leaders. Specifically, MSC boasts the largest orderbook with 2.05 million TEU, while CMA CGM’s orderbook represents 45.5% of its current operational capacity. COSCO Shipping also maintains a substantial orderbook ratio of 38.1% relative to its existing fleet. Some carriers are aggressively expanding through newbuildings, with Regional Container Lines (Thailand) holding orders equivalent to 145.9% of its current capacity, and TS Lines and Wan Hai Lines also recording notable ratios of 72.7% and 67.4%, respectively.

Following a period of market prosperity, leading shipping lines are actively expanding their capacity through newbuilding orders to address decarbonization transitions, alliance restructurings, and future competitive pressures. Despite the massive orderbook size, with some vessels scheduled for delivery as late as 2030, factors such as saturated shipyard capacity, elevated construction costs, and concerns about structural overcapacity are expected to moderate new order activity in 2026. While the industry continues to enjoy growth, stakeholders must prepare for upcoming cyclical adjustments.